Introduction

Market crashes are inevitable.

Whether it’s the 2008 Financial Crisis, the COVID-19 market panic of 2020, or future economic downturns, every investor will face periods when stock prices fall sharply and uncertainty dominates the headlines.

While nobody can accurately predict the next recession, smart investors can prepare for it.

A recession-resistant portfolio isn’t designed to eliminate losses entirely. Instead, it’s structured to reduce risk, preserve capital, maintain steady income, and recover faster when markets rebound.

In this guide, you’ll learn how to build a portfolio that can survive economic downturns, market crashes, inflation shocks, and periods of high uncertainty.

Table of Contents

The Problem: Why Most Investors Lose Money During Market Crashes

Many investors build portfolios during bull markets when stocks seem unstoppable.

Common mistakes include:

- Investing only in growth stocks

- Lack of diversification

- Chasing trending sectors

- Ignoring emergency funds

- Overexposure to risky assets

- Panic selling during downturns

When a recession arrives:

📉 Stock prices fall

📉 Corporate profits decline

📉 Unemployment rises

📉 Consumer spending weakens

📉 Investor confidence disappears

As a result, concentrated portfolios often suffer severe losses.

Example

Imagine two investors:

Investor A

- 100% Technology Stocks

Investor B

- Diversified Portfolio

- Stocks

- Bonds

- Gold

- Cash

During a recession, Investor A may experience a 40-60% decline, while Investor B may experience significantly smaller losses.

The goal isn’t to avoid downturns completely.

The goal is survival.

What Is a Recession-Resistant Portfolio?

A recession-resistant portfolio is designed to:

✅ Protect capital

✅ Generate income

✅ Reduce volatility

✅ Preserve purchasing power

✅ Recover faster after downturns

Think of it as building a financial fortress.

The Solution: Core Principles of Recession Proof Investing

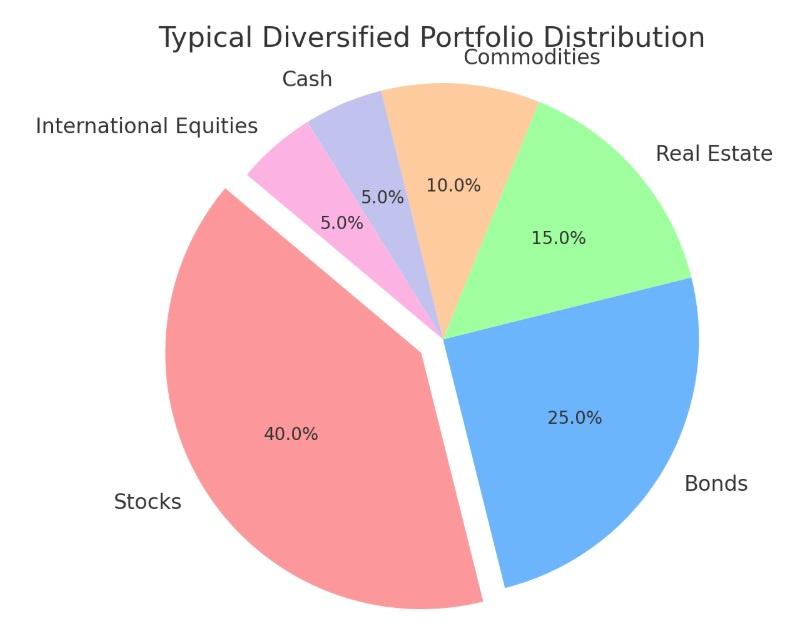

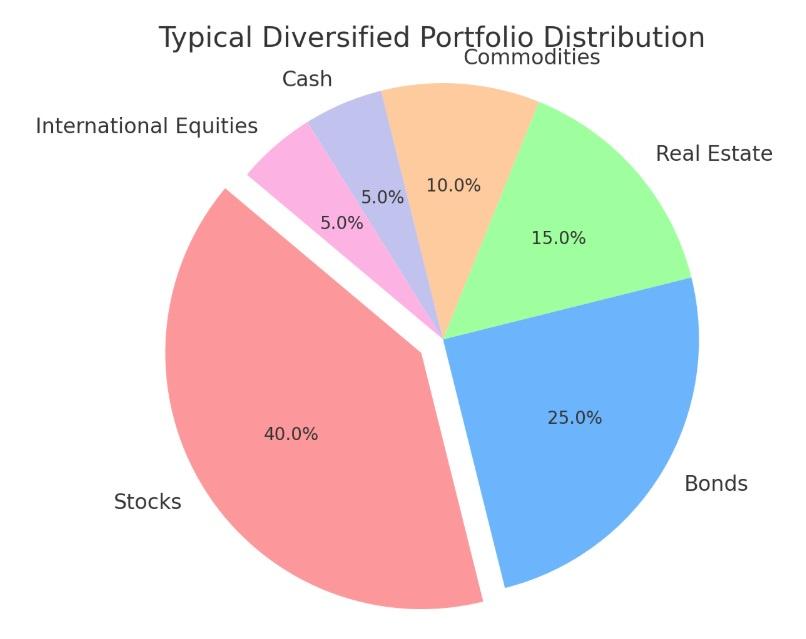

1. Diversification Is Your Best Defense

Never depend on a single asset class.

Spread investments across:

| Asset Class | Purpose |

|---|---|

| Stocks | Growth |

| Bonds | Stability |

| Gold | Inflation hedge |

| Cash | Liquidity |

| REITs | Income |

| International Stocks | Geographic diversification |

Suggested Image

Feature Graphic: Diversified Portfolio Pie Chart

- 50% Stocks

- 20% Bonds

- 10% Gold

- 10% REITs

- 10% Cash

2. Focus on Quality Companies

During recessions, weak companies struggle.

Strong companies survive.

Look for:

- Consistent profits

- Strong cash flow

- Low debt

- Dividend history

- Competitive advantage

Examples

- Microsoft

- Johnson & Johnson

- Procter & Gamble

These businesses continued operating through multiple recessions.

3. Add Defensive Sectors

Some industries remain essential regardless of economic conditions.

Defensive Sectors

| Sector | Why It Holds Up |

| Healthcare | People need medical care |

| Utilities | Electricity demand continues |

| Consumer Staples | Daily necessities remain essential |

| Telecommunications | Internet and communication services |

Suggested Infographic

“Defensive Sectors During Recession”

Icons:

- Medicine

- Electricity

- Groceries

- Internet

4. Maintain an Emergency Cash Reserve

Cash provides flexibility.

Benefits:

- Covers emergencies

- Prevents forced selling

- Creates buying opportunities

Most experts recommend:

Emergency Fund Formula

Monthly Expenses × 6–12 Months

Example:

₹50,000 × 12 = ₹6,00,000

Emergency Fund Target

5. Invest in Bonds

Bonds often perform better when stocks struggle.

Benefits:

- Lower volatility

- Regular income

- Portfolio stabilization

Examples:

- Government Bonds

- Treasury ETFs

- High-Quality Corporate Bonds

Suggested Chart

Stock vs Bond Performance During Market Downturns

(Line Chart)

X-axis: Market Crashes

Y-axis: Portfolio Value

Stocks show greater volatility while bonds remain more stable.

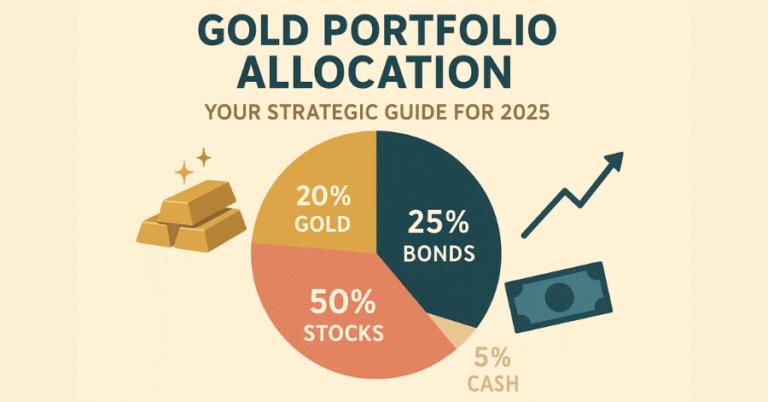

6. Consider Gold as Insurance

Gold has historically acted as a safe-haven asset.

Benefits:

- Inflation protection

- Currency hedge

- Crisis protection

Allocation:

5%-15% of portfolio

Suggested Image

Gold bars with rising inflation graph.

Headline:

“Gold: The Portfolio Insurance Policy”

7. Avoid Excessive Debt

Debt amplifies financial stress during recessions.

Priority order:

- High-interest debt

- Credit cards

- Personal loans

- Margin loans

Reducing debt improves portfolio resilience.

Example Recession-Resistant Portfolios

Conservative Investor

| Asset | Allocation |

| Stocks | 40% |

| Bonds | 35% |

| Gold | 10% |

| Cash | 15% |

Balanced Investor

| Asset | Allocation |

| Stocks | 55% |

| Bonds | 25% |

| Gold | 10% |

| Cash | 10% |

Aggressive Investor

| Asset | Allocation |

| Stocks | 70% |

| Bonds | 15% |

| Gold | 5% |

| Cash | 10% |

Suggested Portfolio Allocation Graphic

Three pie charts side-by-side.

Conservative vs Balanced vs Aggressive.

Historical Lessons From Major Market Crashes

2008 Financial Crisis

S&P 500 decline:

Approximately -57%

Investors with diversified portfolios recovered much faster.

COVID-19 Crash (2020)

Market fell over 30% within weeks.

Investors who remained invested recovered quickly.

Key lesson:

Stay invested.

Inflation Shock (2022)

Growth stocks suffered.

Value stocks, energy, and defensive sectors performed better.

Lesson:

Diversification matters.

The Importance of Rebalancing

Markets constantly change.

Over time, allocations drift.

Example:

Target:

- Stocks 60%

- Bonds 40%

After a bull market:

- Stocks 75%

- Bonds 25%

Risk increases.

Rebalancing restores original allocation.

Recommended frequency:

- Every 6 months

- Annually

Portfolio Stress Test

Ask yourself:

If the market falls 30% tomorrow:

Can I stay invested?

If unemployment rises:

Do I have enough cash reserves?

If inflation reaches 8%:

Will my portfolio keep pace?

If the answer is no, adjustments may be needed.

Recession Portfolio Calculator

Use this simple formula:

Risk Score Formula

Stock Allocation × 1.0

Bond Allocation × 0.4

Gold Allocation × 0.2

Cash Allocation × 0.1

Example:

60% Stocks

20% Bonds

10% Gold

10% Cash

Risk Score

= 60 + 8 + 2 + 1

= 71

Interpretation:

| Score | Risk Level |

| Below 40 | Conservative |

| 40-70 | Moderate |

| Above 70 | Aggressive |

Common Mistakes to Avoid

1. Panic Selling

Temporary losses become permanent.

2. Chasing Hot Stocks

Trends change quickly.

3. Ignoring Diversification

Concentration increases risk.

4. Timing the Market

Extremely difficult to do consistently.

5. Keeping No Cash

Eliminates flexibility.

Frequently Asked Questions

Can a portfolio completely avoid losses during a recession?

No.

The objective is reducing risk and improving recovery potential.

How much cash should I keep?

Typically 6-12 months of living expenses.

Is gold necessary?

Not mandatory, but many investors use 5%-15% for diversification.

Are dividend stocks safer?

They can provide income and often belong to mature businesses.

Should I stop investing during a recession?

Historically, continuing to invest has often produced strong long-term results.

Affiliate Recommendations

Investment Platforms

Recommended categories:

- Discount Brokers

- ETF Investing Platforms

- Robo-Advisors

- Retirement Investment Platforms

Potential affiliate opportunities:

- Brokerage accounts

- ETF investing services

- Portfolio management tools

- Financial planning software

Portfolio Tracking Tools

Useful tools to recommend:

- Portfolio analyzers

- Asset allocation trackers

- Retirement planners

- Budgeting software

These can provide recurring affiliate income while helping readers manage risk effectively.

Final Action Plan

Step 1:

Build an emergency fund.

Step 2:

Diversify across multiple asset classes.

Step 3:

Invest in quality businesses.

Step 4:

Add defensive sectors.

Step 5:

Include bonds and gold.

Step 6:

Rebalance annually.

Step 7:

Stay invested during market volatility.

Conclusion

Market crashes are not a matter of “if” but “when.”

Investors who prepare in advance often weather downturns far better than those who react emotionally.

A recession-resistant portfolio doesn’t guarantee profits or eliminate losses. Instead, it creates a strong foundation capable of surviving economic uncertainty, preserving wealth, generating income, and positioning investors to benefit when markets recover.

By combining diversification, quality investments, defensive sectors, bonds, cash reserves, and disciplined rebalancing, you can build a portfolio that remains resilient through nearly any market environment.

The most successful investors aren’t necessarily those who earn the highest returns during bull markets.

They’re the ones who stay in the game long enough to benefit from decades of compounding.

Build your portfolio for survival first. Growth will follow.

Disclaimer

The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. All investments involve risk, including the potential loss of principal. Past performance does not guarantee future results. Readers should conduct their own research and consult a qualified financial advisor before making any investment decisions. RicherGuide.com and the author are not responsible for any financial losses resulting from the use of this information.